Why the Washington state income tax is unconstitutional

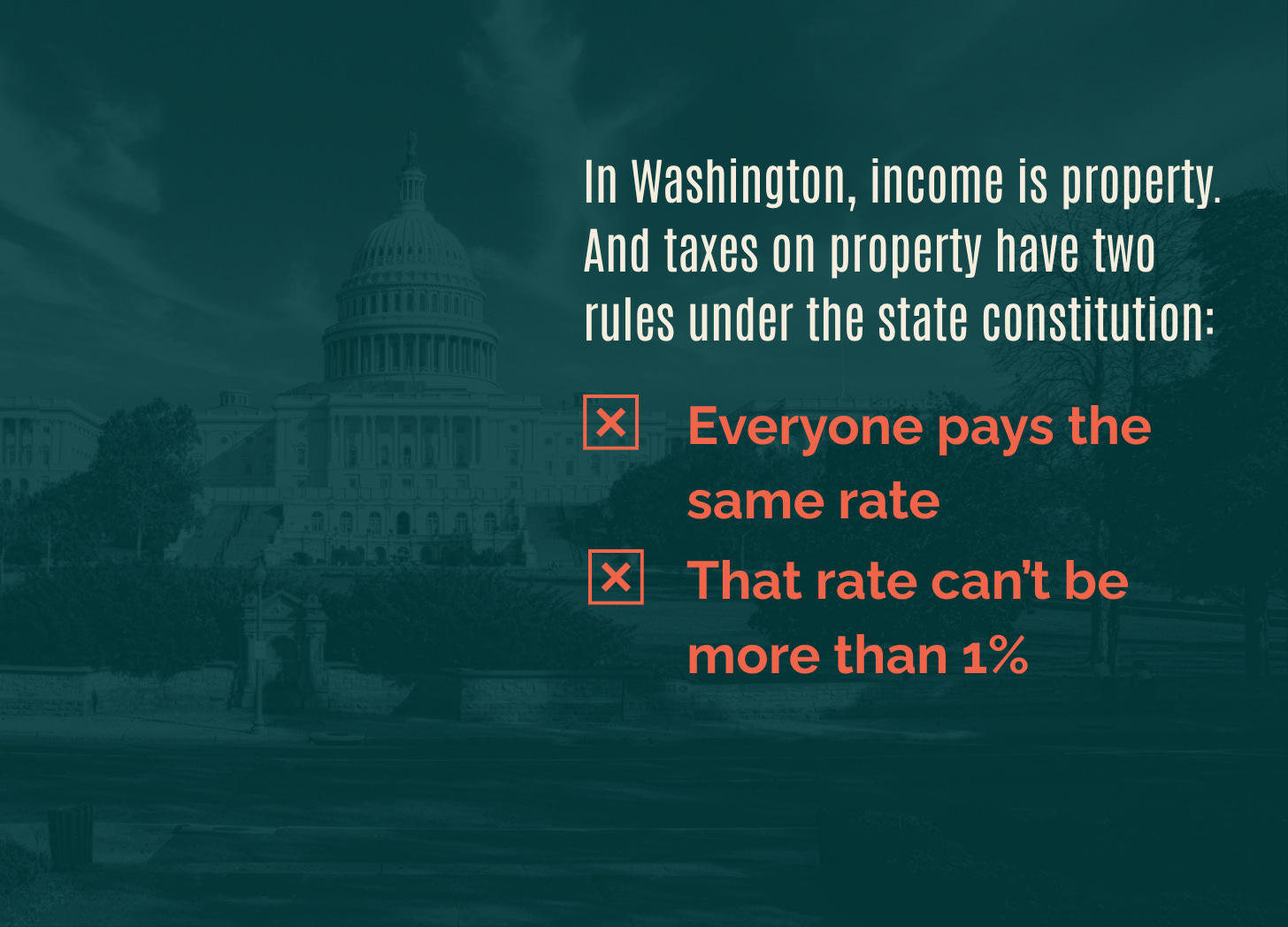

Washington’s constitution has long treated income as property—and that classification comes with strict limits. Property taxes in Washington must meet two clear requirements: they must be uniform, meaning the same type of property is taxed at the same rate, and they cannot exceed a 1% cap.

The proposed state income tax violates both.

First, it applies only to certain individuals—those earning above $1 million—while exempting others entirely. That is not uniform taxation. Second, the rate itself is far beyond the constitutional limit, reaching roughly 10%, which is ten times higher than what is allowed for property.

Supporters argue the policy targets only high earners, but the legal issue isn’t who is taxed—it’s how. Under the constitution, income as property must be treated consistently and within strict boundaries.

The constitution can be amended, of course, but that requires a vote of the people. Washington voters have rejected an income tax the last ten times they’ve been given the choice. This time, proponents avoided that process—rejecting amendments that would have allowed voters to weigh in directly.

As a retiree, this tax on "millionaires" won't affect me directly, But I am still opposed to it, because this "eat the rich" approach will only drive high income (and high tax paying) people OUT of our state.

Passing an un-Constitutional income tax on people with high incomes will only convince them that it is in their best interest to move OUT of our state, And when they leave, Washington state will no longer be able to collect ANTHING from them.

So, this "millionaires' tax" will actually result in a net LOSS of tax revenue for our state. If you pass laws to over-tax "the rich" they will just move elsewhere. They can afford to relocate, and THEY WILL.

Massachusetts and California are two states that have tried this, and they are both seeing a mass-exodus of wealth from their taxing jurisdictions.

Washington should NOT follow their example.

When your tax policy drives the people paying the MOST in taxes away, it is us regular folks who end up paying for it. If the state can't collect more from the rich, they will end up collecting it from the rest of us.

Vote against this "eat the rich", class-warfare money grab. Or we'll ALL pay the price...

Mr. Counts is right at the moment it won't affect him directly, AT THIS TIME. Unfortunately it will affect him indirectly.

First they came for the billionaires. And I did nothing. Then they came for the millionaires and I did nothing.

Then they came for those making less than millions. And an eye on my retirement account along with other retirees.

Why anyone who can afford to move stays on the left coast is beyond me.